This article contains affiliate links. If you purchase or book through these links, we may earn a commission at no additional cost to you.

We all know the feeling. You are staring at a screen that is buffering for the fifth time in ten minutes. The battery life on your current device has dwindled from a respectable eight hours to a pathetic forty-five minutes.

You need an upgrade. That part is undeniable. But then, you click over to the checkout cart, and reality hits you like a brick wall. The sticker shock of a brand-new Apple iPad or a high-performance HP Laptop is enough to make anyone slam their laptop shut.

But what if the problem isn’t the price of the technology, but the way we have been conditioned to pay for it?

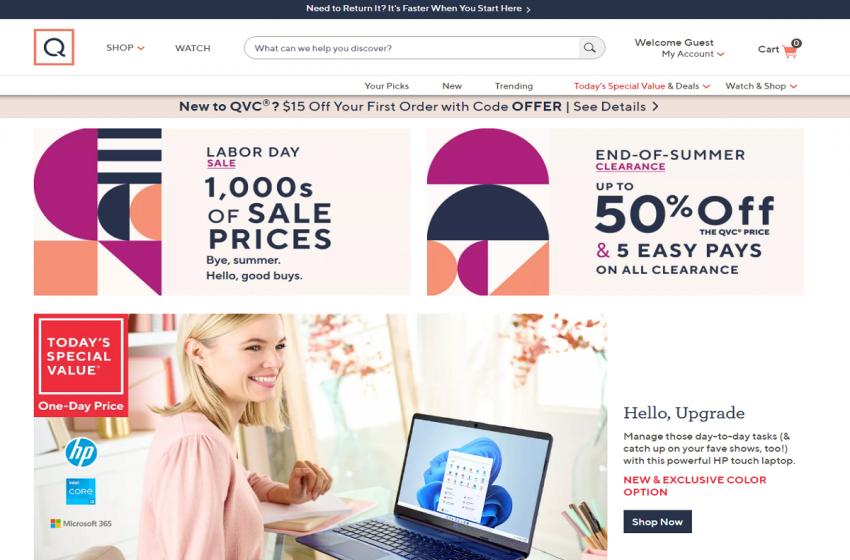

Welcome to the best-kept secret in the tech-buying world: QVC. Yes, the same network your family might watch for kitchen gadgets and holiday decor is actually sitting on one of the most powerful, consumer-friendly financing models in the electronics industry. If you want to upgrade your tech without destroying your cash flow, you need to understand how to maximize QVC’s “5 Easy Pays” system.

The Pitfalls of Traditional Tech Financing

Before we dive into the QVC method, it is crucial to understand why the traditional methods of buying high-end tech are fundamentally flawed for most young professionals, students, and budget-conscious consumers.

When you go to a big-box retailer or a major brand’s website to buy an HP Laptop or an iPad, you are generally presented with three terrible options if you cannot pay in full:

- The High-Interest Credit Card: You put the $1,200 laptop on your standard credit card. If you don’t pay it off immediately, you are suddenly hit with 18% to 24% APR. By the time you actually pay off the machine, that $1,200 laptop has cost you $1,600.

- The Store Credit Card Trap: The retailer offers you “0% financing for 12 months!” But there is a catch. To get it, you have to consent to a hard inquiry on your credit report, which dings your score. Then, if you miss a single payment, or fail to pay off the entire balance by the end of the promotional period, you are hit with deferred interest retroactively applied from the date of purchase.

- The Third-Party BNPL (Buy Now, Pay Later) Apps: These micro-loan apps have surged in popularity, but they often come with stringent approval odds, hidden late fees, and very short repayment windows (usually requiring the balance to be paid in just six weeks).

None of these options are genuinely designed with the consumer’s financial health in mind. They are designed to trap you in debt. This is precisely why the QVC model is such a profound breath of fresh air.

The QVC Secret Weapon: Deep Dive into “5 Easy Pays”

“Easy Pay” is exactly what it sounds like. QVC takes the total price of the item, including shipping and tax, and divides it into five equal, manageable monthly installments.

Here is why this mechanic is uniquely beneficial and fundamentally different from predatory financing:

1. Zero Interest, Ever

This is the most critical factor. Easy Pay is not a loan. It is not a financing plan tied to an APR. There is absolutely no interest charged on your purchase. If the iPad costs $800, you pay exactly $800, just spread over five months. Every single penny of your monthly payment goes toward the principal balance of the device.

2. No Credit Check Required

When you use store financing or apply for a tech brand’s credit card, they run a hard pull on your credit history. If you are a student who hasn’t built up a massive credit file yet, you might be denied outright. With QVC’s Easy Pay, there is no credit check. You are not applying for a new line of credit. As long as you have a valid, major credit card or debit card that can process the initial payment, you are generally good to go.

3. Splitting the Bill Across Your Existing Cards

Instead of opening a new, dangerous store card, Easy Pay utilizes the financial tools you already have in your wallet. You simply check out using your standard Visa, Mastercard, American Express, or Discover. QVC bills your card for the first installment on the day your item ships. Then, for the next four months, they automatically bill that exact same card on the same day of the month for the remaining installments.

It is seamless, it is predictable, and it leverages your existing banking setup without requiring you to jump through bureaucratic hoops.

Real-World Scenarios: The Math That Makes Sense

Let’s look at how this changes the game for purchasing premium devices.

Scenario A: The Premium HP Laptop

Imagine you are entering a heavy academic semester, or perhaps you are launching a side hustle that requires serious multitasking, graphic design, and video rendering. You need a powerhouse machine. You find a high-end HP Laptop bundle on QVC retailing for $1,000.

- Traditional Route: You drain $1,000 out of your checking account on a random Tuesday. Your rent is due next week, and now you are stressing about buying groceries because your cash flow has been completely decimated.

- The QVC Route: You select “5 Easy Pays.” You pay $200 today. The laptop ships immediately. You get the machine, you start doing your coursework, you start building your digital business, and you simply pay $200 a month for the next four months. You still have $800 in your bank account today to cover your living expenses.

Scenario B: The Apple iPad Ecosystem

Tech gadget fans know that the iPad is no longer just a screen for watching movies; it is a dedicated productivity machine, a digital canvas, and the ultimate smart-home controller. But buying a new iPad, plus the Apple Pencil, plus a keyboard case, can easily run you $850.

- Traditional Route: You put $850 on a credit card, intending to pay it off, but life happens. You carry the balance for a year, accumulating $150 in interest charges.

- The QVC Route: You utilize Easy Pay. You pay $170 today. The brand-new iPad arrives at your door. Next month, you pay $170. You enjoy zero interest. The device is yours immediately, but the financial burden is distributed to match your monthly income.

Why This is a Game-Changer for Students

For students, cash flow is king. Financial aid, part-time job paychecks, and stipends do not arrive in massive, limitless waves. They arrive on strict schedules.

When a student’s laptop dies in the middle of midterms, it is a catastrophic emergency. They do not have the time to save up for three months to buy a replacement. They need a laptop tomorrow so they can finish their assignments. But they also cannot afford to drop their entire month’s rent on a new machine.

QVC’s Easy Pay acts as a financial shock absorber. It allows students to acquire the necessary, high-tier educational tools immediately without triggering a financial crisis. Furthermore, QVC frequently bundles their tech. When you buy an HP laptop or an iPad from QVC, it rarely comes alone. They often bundle in essential software, carrying sleeves, wireless mice, or tech support packages. For a student, getting a complete “ready-to-work” ecosystem in one split-payment purchase is a massive time and stress saver.

How to Maximize the QVC Advantage

To truly master the art of upgrading your tech via QVC, keep these strategic tips in mind:

- Watch for “Today’s Special Value” (TSV): QVC heavily discounts one specific item for 24 hours. When a top-tier HP Laptop or an Apple iPad is the TSV, the base price is slashed to compete with major electronics retailers, making the 5 Easy Pays even more affordable.

- Leverage the Bundles: As mentioned, QVC rarely sells a naked device. Evaluate the included software and accessories. If the iPad comes with premium Bluetooth headphones and a protective case, factor those savings into your overall tech budget.

- Time Your Upgrades: Because you are splitting payments, time your purchases around predictable income. If you know you have steady income for the next five months, lock in the Easy Pay.

Upgrade Without the Anxiety

We rely on our laptops and tablets for everything. They are our connection to our universities, our workplaces, our creative outlets, and our social lives. You should not have to choose between financial stability and a device that actually functions the way you need it to.

By utilizing QVC’s 5 Easy Pays, you bypass the trap of high-interest credit cards, avoid the ding of unnecessary credit checks, and protect your monthly cash flow. You get the HP laptop that can handle your heaviest software. You get the iPad that brings your digital planning to life. And best of all, you get to unbox your new technology with pure excitement, completely free of buyer’s guilt.

Frequently Asked Questions

How does Easy Pay work when buying tech?

Easy Pay allows you to split the total cost into smaller monthly payments, making it easier to afford higher-quality devices without a large upfront expense.

Is financing a laptop or tablet a good idea?

It can be, especially if you need reliable tech for work or study. Just ensure the payment plan fits comfortably within your budget.

What should I look for when buying a laptop or tablet?

Focus on performance (RAM and processor), battery life, display quality, and storage based on your specific needs.